- EXPERIENCED LAW FIRM IN TOLEDO, OH

- (419) 662-3100

Challenges of Inheriting Across Multiple States

Estate Planning Across State Lines

Multi-state inheritance can be complex due to different states’ varying laws and regulations governing asset transfer upon death. Each state has its own probate rules, tax structures, and restrictions on how property is distributed, which means an estate with assets across multiple states may need to go through separate probate proceedings—each with its own timelines, costs, and legal requirements.

For example, one state might recognize certain types of wills or allow for a simplified probate process, while another may have stricter standards or not identify specific documents at all. These differences can create delays, increase administrative burdens, and lead to conflicts among beneficiaries.

Understanding these complexities is crucial for effective estate planning. It allows individuals to develop strategies, such as setting up trusts or legal entities, to minimize complications, reduce tax burdens, and ensure their assets are distributed according to their wishes without unnecessary legal hurdles.

Grasping Multi-State Probate

Probate is a legal process that occurs after someone passes away. It involves validating their will (if one exists), settling debts and taxes, and distributing the remaining assets to beneficiaries. When an individual owns assets in different states, probate becomes more complicated because each state has its own probate laws and requirements. In such cases, the estate may need to undergo ancillary probate, a separate probate proceeding in each state where the deceased owned property.

Ancillary probate ensures that state-specific legal protocols are followed for those assets. Still, it can significantly affect the inheritance process by increasing the time, costs, and administrative burden required to settle the estate. Executors may need to hire attorneys in each state, manage varying timelines, and pay court fees in multiple jurisdictions. This leads to a more prolonged and expensive process that could delay beneficiaries from receiving their inheritance.

Variations in State Laws Affecting Inheritance

State laws on inheritance and probate vary significantly, which can complicate the administration of estates with assets in multiple states. These differences affect how wills are validated, how assets are distributed if someone dies without a will (intestate), and how the probate process is conducted. For instance, community property states and common law states handle marital property differently, leading to distinct outcomes for asset distribution.

Moreover, states differ in their acceptance of specific types of wills, such as nuncupative (oral) wills or holographic (handwritten) wills. Key differences include:

- Wills and Probate Procedures: States have different rules for validating a will, including requirements for witness signatures, notarization, and specific language. Some states offer streamlined probate processes, while others require more comprehensive court oversight.

- Intestate Succession Laws: If a person dies without a valid will, each state has laws on distributing assets among surviving relatives. Some states prioritize spouses, while others divide assets equally among children, parents, and siblings.

- Community Property vs. Common Law States: In community property states, assets acquired during marriage are generally considered jointly owned and are split equally upon death. In contrast, common law states may recognize more individually owned property, which affects how assets are divided in probate.

- Recognition of Nuncupative and Holographic Wills: Some states accept nuncupative (oral) wills made under urgent circumstances, like imminent death, while others do not. Similarly, holographic (handwritten) wills are valid in certain states if they meet specific criteria but are not recognized in others, which can complicate cross-state inheritance.

Tax Implications of Multi-State Inheritance

Estate tax, inheritance tax, and income tax on inherited assets are three types of taxes that can affect beneficiaries, and each can vary significantly from state to state. Estate tax is typically levied on the total value of a deceased person’s estate before distribution, while inheritance tax is paid by beneficiaries on the assets they receive.

Some states impose both, one, or neither, creating different tax burdens for beneficiaries depending on where the deceased and the property are located. Additionally, income tax may apply to certain inherited assets, such as retirement accounts.

Beneficiaries can employ strategies to minimize these tax liabilities, such as creating trusts to avoid probate, using gifting during the estate holder’s lifetime to reduce the taxable estate, or holding property through entities like LLCs that can offer tax benefits and simplify asset transfer across states.

Challenges for Executors and Beneficiaries

An executor handling an estate with assets in multiple states must manage different probate processes, each with state-specific laws and requirements. This often involves filing for probate separately in each state where the deceased owned property, a process known as ancillary probate. As a result, the executor may need to coordinate with multiple attorneys, manage different court procedures, and navigate various timelines and costs, all of which can lead to significant delays. These delays and the legal complexities can cause frustration among beneficiaries who are waiting for their inheritance.

Additionally, differences in state laws, such as those governing asset distribution or taxes, can lead to misunderstandings and conflicts among beneficiaries, particularly if there are disagreements about the fairness of the distribution, asset valuations, or the terms of the will.

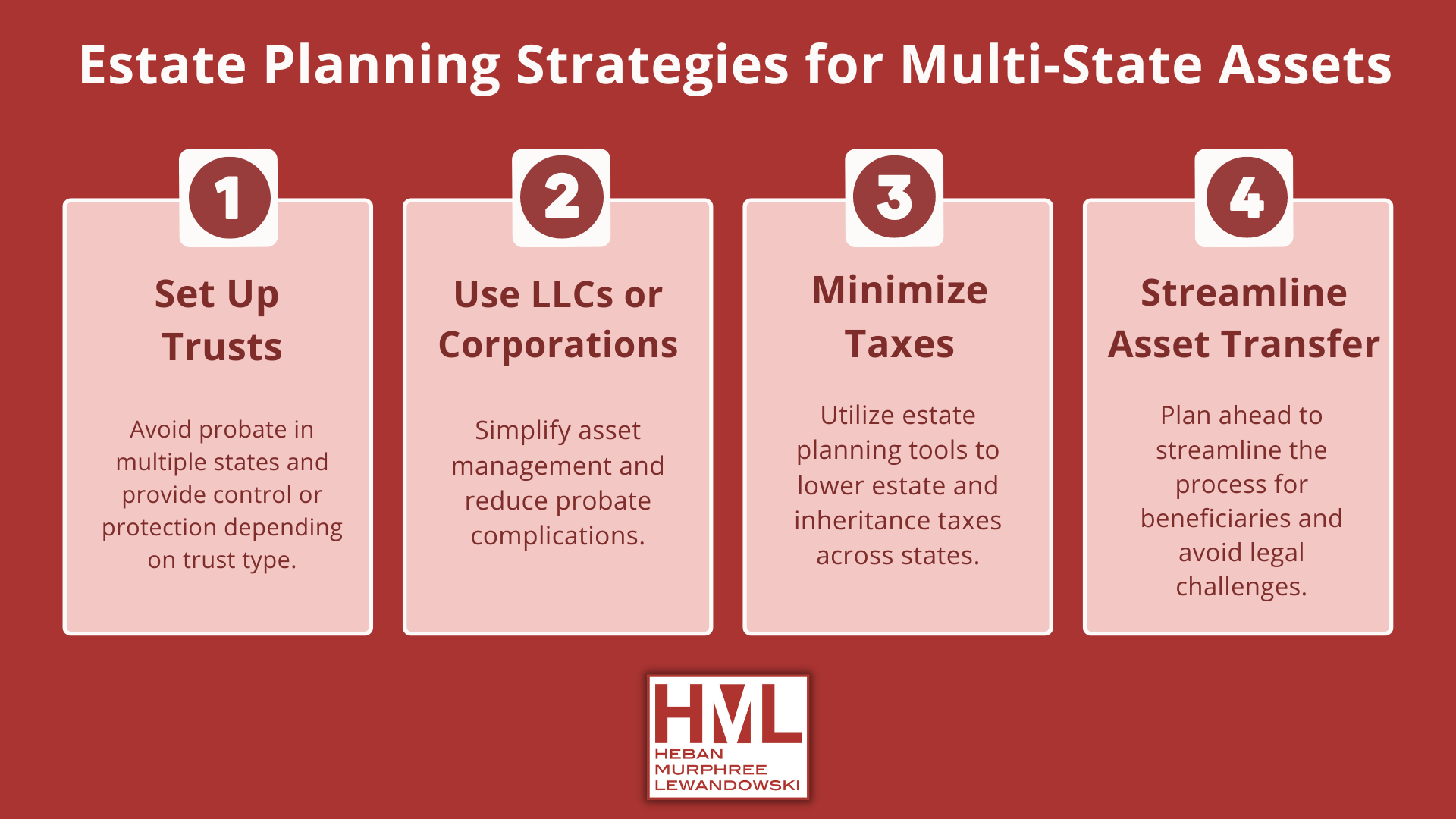

Strategies for Estate Planning with Multi-State Assets

Thorough estate planning is essential for handling the complexities of multi-state inheritance, as it helps simplify the transfer of assets and reduces legal challenges across different states. Using effective estate planning tools, individuals can avoid multiple probate proceedings, minimize tax burdens, and ensure a smoother process for beneficiaries.

Some key strategies include:

- Establishing Revocable and Irrevocable Trusts: Trusts allow assets to pass directly to beneficiaries without going through probate, eliminating the need for separate probate processes in each state where the property is owned. Revocable trusts provide flexibility and control during the estate owner’s lifetime, while irrevocable trusts offer stronger protection against taxes and creditors.

- Utilizing Legal Entities like LLCs or Corporations: Holding property through an LLC or corporation can streamline asset management and inheritance across state lines. This approach consolidates ownership under a single legal entity, reducing probate complexities and offering potential tax advantages and liability protection.

Important Notes for Beneficiaries

Beneficiaries inheriting from an estate with assets in multiple states should be aware that the process may be more complex and time-consuming due to varying state probate laws and requirements.

Beneficiaries need to communicate clearly with the executor and any involved legal professionals to stay informed about the status of the probate proceedings in each state. They should ask questions about timelines, potential delays, and state-specific tax implications that could affect their inheritance, such as estate, inheritance, or income taxes.

Need Legal Help?

Different states have different legal requirements, and having local expertise can help prevent delays and avoid unnecessary complications. Sometimes, this may mean hiring separate attorneys in other states to handle specific probate issues effectively.

Our team can help you create a comprehensive estate plan that considers all these factors, setting up trusts or other strategies to minimize taxes and simplify the process for your loved ones.

To make sure your estate is managed smoothly and in line with your wishes, call us at (419) 662-3100 to schedule a consultation and get started with expert, personalized legal guidance.