- EXPERIENCED LAW FIRM IN TOLEDO, OH

- (419) 662-3100

What Are Beneficiary Designations?

Legal Strategies for Ohio Agricultural Operations

July 3, 2024

Guide to Farm Estate Planning and Succession

September 2, 2024

Key Steps for Secure Estate Planning

Beneficiary designations allow individuals to name specific beneficiaries to receive certain assets directly upon death, bypassing the probate process and overriding any instructions in a will or trust.

These designations are commonly used for various types of accounts and assets, including life insurance policies, retirement accounts such as 401(k)s and IRAs, Payable on Death (POD) or Transfer on Death (TOD) bank accounts, stocks and bonds, and annuities. By designating beneficiaries, the account owner guarantees that the assets are transferred directly to the named individuals or entities, facilitating a quicker and more efficient transfer of wealth and reducing the administrative burden and costs associated with probate.

Legal Framework in Ohio

Ohio Revised Code §2131.10 sets the rules for the validity and enforcement of beneficiary designations in the state. It states that beneficiary designations on life insurance policies, annuity contracts, and similar accounts take precedence over any conflicting provisions in wills or trusts. This means that assets with named beneficiaries are transferred directly to those individuals or entities, bypassing the probate process and any instructions specified in a will or trust.

The main difference between beneficiary designations and wills or trusts is in how assets are transferred: beneficiary designations allow for a quick, direct transfer of specific assets outside of probate, while wills and trusts usually involve a more detailed estate plan that includes all assets and may require probate to validate and carry out the decedent’s wishes.

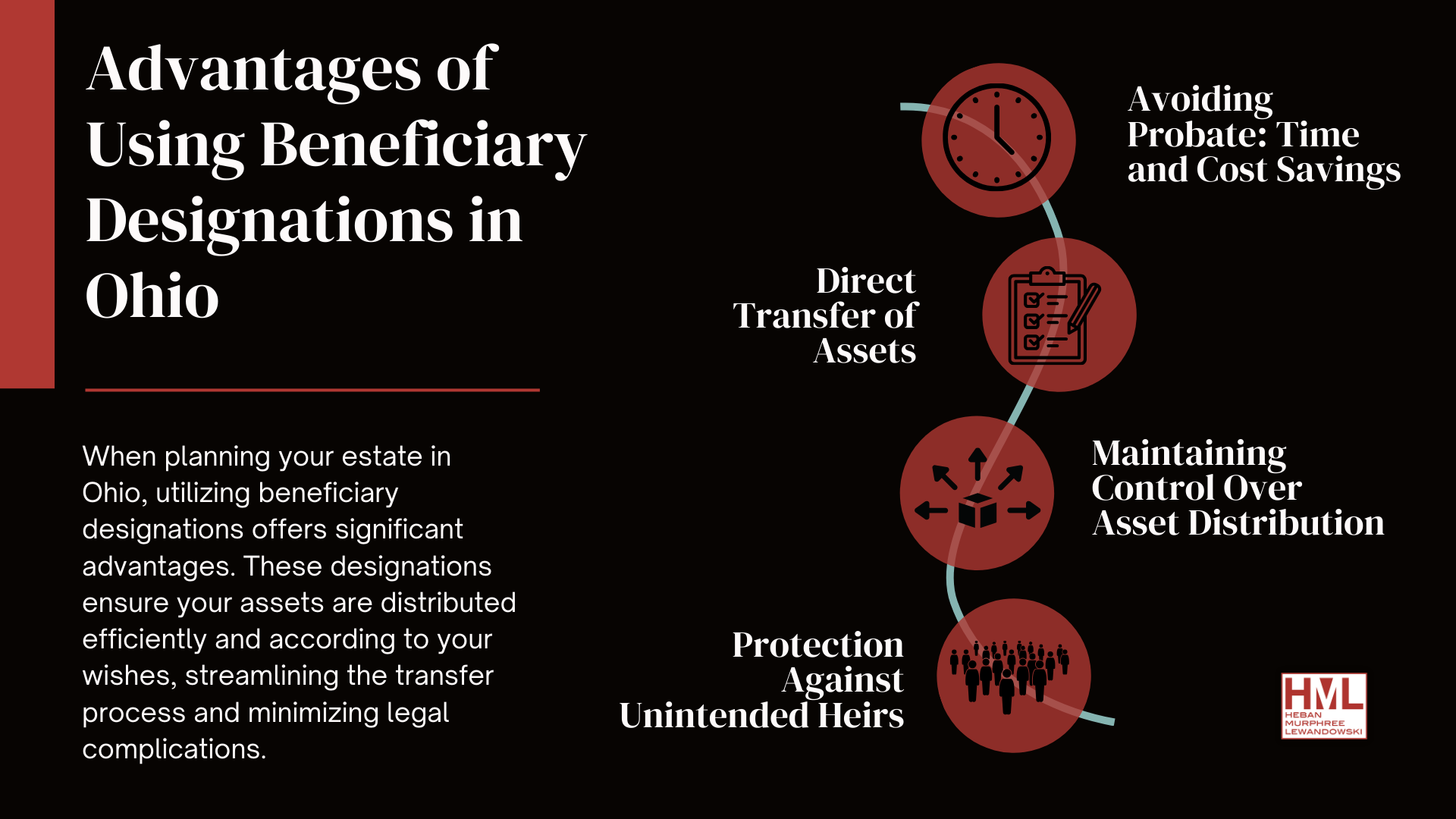

Benefits of Using Beneficiary Designations

Beneficiary designations offer significant advantages in estate planning, primarily through avoiding probate, facilitating the direct transfer of assets, and maintaining control over asset distribution. Here’s how:

- Avoiding probate: time and cost savings: By designating beneficiaries, you can bypass the probate process, which is often time-consuming and expensive, ensuring that your assets are transferred quickly and efficiently to your heirs.

- Direct transfer of assets to beneficiaries: Beneficiary designations enable a seamless transfer of assets directly to the named individuals or entities upon your death, eliminating the need for court involvement and reducing administrative burdens.

- Control over asset distribution: With beneficiary designations, you maintain precise control over who receives specific assets, ensuring that your estate planning wishes are honored exactly as intended, without the delays and complications that can arise from probate.

Types of Beneficiary Designations

It’s important to understand the distinctions between primary and contingent beneficiaries, per stirpes and per capita distribution, and individuals versus trusts or legal entities when designating beneficiaries.

Primary beneficiaries are the first in line to receive assets upon the account holder’s death, while contingent beneficiaries are designated to inherit if the primary beneficiaries predecease the account holder. Distribution methods also vary: per stirpes means a deceased beneficiary’s descendants will inherit their share, ensuring assets stay within the family lineage, whereas per capita distribution divides the assets equally among surviving beneficiaries.

Furthermore, beneficiaries can be individuals or legal entities such as trusts, corporations, or limited liability companies. Designating a trust as a beneficiary can offer benefits like asset protection and management flexibility, particularly for minor or special needs beneficiaries. At the same time, individual designations are straightforward and directly transfer assets to named persons.

Common Mistakes and How to Avoid Them

Neglecting to update beneficiary designations can lead to unintended consequences, such as assets being passed to an ex-spouse or deceased individual, which may not align with your current estate planning intentions.

Naming minors as beneficiaries without setting up a trust can also cause complications, as minors cannot directly inherit assets, necessitating the appointment of a legal guardian to manage the inheritance until they reach adulthood. Failing to consider tax implications can result in unnecessary tax burdens for your beneficiaries, reducing the overall value of their inheritance.

Moreover, overlooking the designation of contingent beneficiaries can create issues if the primary beneficiaries predecease you, potentially causing the assets to revert to your estate and go through probate. Regularly reviewing and updating your beneficiary designations ensures that your assets are distributed according to your current wishes and most efficiently.

How Beneficiary Designations Work in Ohio

This guide outlines the steps and requirements for a valid beneficiary designation and explains its impact on asset transfer.

- Step 1: Identify Eligible Assets – Determine which assets can have beneficiary designations, including life insurance policies, retirement accounts, POD/TOD bank accounts, stocks, bonds, and annuities.

- Step 2: Choose Your Beneficiaries – Decide who will receive the assets. You can name individuals, trusts, or legal entities. Consider both primary and contingent beneficiaries for different scenarios.

- Step 3: Complete the Beneficiary Designation Form – Obtain and accurately fill out the beneficiary designation form from your financial institution or account holder.

- Step 4: Meet Legal Requirements—Ensure the form is valid by signing and dating it and notarizing it if necessary. If necessary, specify details like the percentage each beneficiary will receive.

- Step 5: Submit and Confirm – Submit the form to the appropriate institution and confirm the designation by checking your account statements or contacting the institution.

Coordination with Other Estate Planning Tools

Integrating beneficiary designations with your wills and trusts is necessary for a well-rounded estate plan. It ensures that all your asset distributions are coordinated and reflect your wishes. Doing so can avoid conflicts and gaps, ensuring your assets are passed on smoothly and efficiently.

An all-inclusive estate plan that keeps everything consistent across all documents also minimizes the risk of legal disputes among your heirs, protects your assets from creditors, and addresses special needs like tax planning and care for minors or beneficiaries with disabilities.

Practical Tips for Ohio Residents

Regularly reviewing and updating your beneficiary designations is crucial to ensure they reflect your current wishes and life circumstances, such as marriage, divorce, or the birth of a child. Seeking professional advice from estate planning attorneys can provide valuable guidance in making informed decisions and avoiding common pitfalls.

In addition, keeping thorough and accurate records of all your beneficiary designations helps prevent misunderstandings and ensures that your assets are distributed according to your plans.

Need Legal Help?

Heban, Murphree & Lewandowski, LLC is a leading probate law firm in Toledo, Ohio. We offer expert guidance on beneficiary designations and comprehensive estate planning. With over 100 years of combined legal experience, our team specializes in ensuring your assets are distributed according to your wishes, avoiding probate, and addressing all aspects of your estate plan.

Contact us to schedule a consultation and learn how our expertise can help you achieve your estate planning goals with confidence.